Share Buybacks

What share buybacks are, why they matter, and when they create or destroy shareholder value.

A share buyback may look like good news.

The company buys back its own shares, there are fewer shares outstanding, and your ownership of the business increases without you doing anything. Sounds good, right?

Careful: there may be a catch.

A buyback can be one of the smartest ways to create shareholder value, or a very elegant way to destroy it while everyone celebrates that EPS has gone up. It all depends on the price paid, where the money comes from, and what alternatives the company had for using that capital. And that is not always as obvious as it seems.

Warren Buffett put it very directly:

In repurchase decisions, price is all-important.

Warren Buffett

Important: This text is a fragment of my original text that you can find at https://www.jeravalue.com/en/blog/buybacks . The original blog contains interactive widgets, contextual information and the full version.

What is a buyback for?

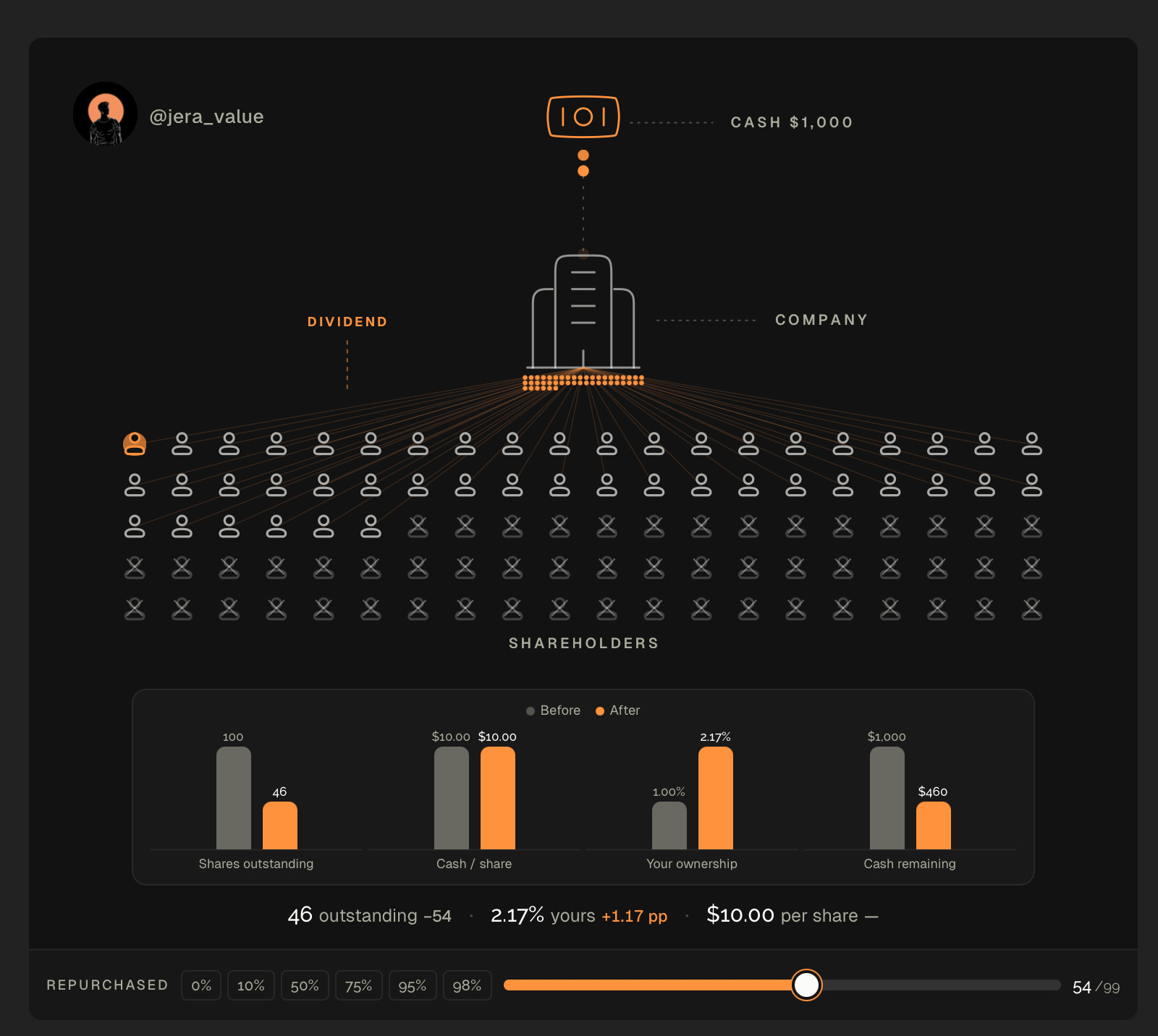

Imagine a company is divided into 100 shares and you own 1. That means you own 1% of the business. Now imagine the company buys back 10 shares and reduces the number of shares outstanding. Before, there were 100 shares. Now there are 90. You still own 1 share, but that same share now represents a larger part of the company. Before, you owned 1%. Now you own roughly 1.1%.

Your number of shares does not change. What changes is the denominator.

When the number of shares falls, each remaining share represents a larger portion of the business. That is why buybacks can be useful. But this is where many people oversimplify.

A buyback does not automatically improve the business.

It does not increase sales, improve the product, make customers happier, or turn a bad company into a good one. All it does is change how ownership is distributed among the shareholders who remain. That is why buybacks can create value, but they can also destroy it. And that is why they should be analyzed much more carefully than they usually are on the surface.

Why do buybacks matter?

Buybacks matter because, at their core, they are a capital allocation decision.

Every euro a company uses to buy back shares is a euro it does not use to invest in the business, pay down debt, make acquisitions, pay dividends, or simply keep cash. That is why a buyback should not be analyzed as a simple trick to reduce the number of shares. It should be analyzed like any other investment.

The question is not: “Did the company buy back shares?”

The question is: “Did the company buy them back well?”

If the company buys back shares below their fair value, using cash it truly does not need and without sacrificing better opportunities, it can create a lot of value. If it buys back shares at an expensive price, with excessive debt, or just to dress up EPS, it can destroy value even if the share count falls.

The basic logic is this:

Value created ≈ (fair value per share − price paid per share) × shares repurchased

If the company pays less than the shares are worth, the remaining shareholder wins. If it pays more, the remaining shareholder loses. It is simple and complex at the same time, because estimating fair value is never trivial.

The test of a good buyback

A good buyback usually passes three filters: price, financing, and opportunity cost.

1. The price paid

This is the most important factor.

A buyback creates value when a company buys its own shares for less than they are really worth. And it destroys value when it buys them for more than they are worth. It sounds obvious, but this is where most of the confusion starts. The fact that the number of shares goes down does not automatically mean value has been created. It only means shares have been bought.

The real question is: were they bought cheaply?

HOW DO YOU KNOW IF THE STOCK IS CHEAP?

This question could fill an entire article. In fact, a big part of investing is precisely about trying to answer it. In practice, the analyst needs to estimate the fair value of the company and compare it with the price at which the company is buying back shares. In hindsight, it is much easier to see, because you can observe whether several years later the stock is clearly trading above or below the price at which the company bought back shares.

Example 1 - BUYING BACK SHARES BELOW NAV

A very common case is when a company trades below its NAV.

Imagine a company with a NAV of $100 per share, but whose stock trades at $70. If the company buys back shares at $70, it is spending $70 to buy something worth $100. That is very good for the shareholders who remain.

Let’s use simple numbers. Suppose the company has 100 shares, $100 of NAV per share, and therefore $10,000 of total NAV. Now it buys back 10 shares at $70 each and spends $700 of cash. After the buyback, the company has $9,300 of total NAV and 90 shares outstanding. The new NAV per share is 9,300 / 90 = $103.33.

Before, each share represented $100 of NAV. Afterward, each share represents $103.33. The reason is simple: the company bought something worth $100 while paying only $70.

That is why buybacks can be especially powerful in holding companies, real estate companies, asset-heavy businesses, and closed-end funds that trade at wide discounts. In those cases, the math can be quite clear.

That said, the NAV has to be reasonably reliable. If the assets are overvalued, hard to sell, or the balance sheet hides problems, the discount may be deserved. Buying back shares below an inflated NAV does not create value; it only looks like it does.

Example 2 - THE OPPOSITE EXAMPLE

Now imagine the opposite situation. That same company is worth roughly $100 per share, but management buys back shares at $130. Here it is spending $130 to buy something worth $100. That destroys value.

Back to the numbers. The company has 100 shares, $100 of value per share, and $10,000 of total value. It buys back 10 shares at $130 each and spends $1,300. After the buyback, there is $8,700 of total value left and 90 shares outstanding. Value per share falls to 8,700 / 90 = $96.67.

Before, each share was worth $100. Afterward, it is worth $96.67. The number of shares has fallen, but value per share has fallen too.

The press release may sound good and EPS may even improve, but economically, shareholders have lost value. That is why the first question should always be the same: is management buying back shares at a price that makes sense?

The interesting part is that a good buyback does not only improve value per share once. If a company buys back shares cheaply on a recurring basis, the effect can compound over time. It is not magic. It is well-allocated capital, repeated for years.

The larger the discount and the longer the company can repeat the operation without damaging the business, the more powerful the effect is for the shareholder who remains.

2. Where the money comes from

The second question is where the money comes from.

Not all buybacks are financed in the same way. The best kind of buyback is one funded with excess cash. In other words, the company has already maintained the business, funded the necessary capex, invested in attractive projects, protected the balance sheet, and still has money left over. In that case, using part of that extra cash to buy back undervalued shares can be perfectly rational.

<Text continues>

As mentioned, this text is a fragment of my original text that you can find at https://www.jeravalue.com/en/blog/buybacks . The original blog contains interactive widgets, contextual information and the full version.

Check it out, you are going to love it!